Key Word(s): Random Forests, Boosting

Random Forests and Gradient Boosted Regression Trees¶

We will look here into the practicalities of fitting random forests and GBRT. These involve out-of-bound estmates and cross-validation, and how you might want to deal with hyperparameters in these models. Along the way we will play a little bit with different loss functions, so that you start thinking about what goes in general into cooking up a machine learning model.

%matplotlib inline

import numpy as np

import scipy as sp

import matplotlib as mpl

import matplotlib.cm as cm

import matplotlib.pyplot as plt

import pandas as pd

pd.set_option('display.width', 500)

pd.set_option('display.max_columns', 100)

pd.set_option('display.notebook_repr_html', True)

import seaborn.apionly as sns

sns.set_style("whitegrid")

sns.set_context("poster")

Dataset¶

First, the data. This one is built into sklearn, its a dataset about california housing prices. Its quite skewed as we shall see.

from sklearn.datasets.california_housing import fetch_california_housing

cal_housing = fetch_california_housing()

cal_housing

from sklearn.model_selection import train_test_split

# split 80/20 train-test

Xtrain, Xtest, ytrain, ytest = train_test_split(cal_housing.data,

cal_housing.target,

test_size=0.2)

names = cal_housing.feature_names

df = pd.DataFrame(data=Xtrain, columns=names)

df['MedHouseVal'] = ytrain

df.hist(column=['Latitude', 'Longitude', 'MedInc', 'MedHouseVal'])

Notice the high bump in the median house value. why do you think that is? How might you model it?

df.head()

df.shape

General Trees¶

We could use a simple Decision Tree regressor to fit such a model. Thats not the aim of this lab, so we'll run one such model without any cross-validation or regularization.

This is what you ought to keep in mind about decision trees.

from the docs:

max_depth : int or None, optional (default=None)

The maximum depth of the tree. If None, then nodes are expanded until all leaves are pure or until all leaves contain less than min_samples_split samples.

min_samples_split : int, float, optional (default=2)- The deeper the tree, the more prone you are to overfitting.

- The smaller

min_samples_split, the more the overfitting. One may usemin_samples_leafinstead. More samples per leaf, the higher the bias.

from sklearn.tree import DecisionTreeRegressor

x = np.arange(0, 2*np.pi, 0.1)

y = np.sin(x) + 0.1*np.random.normal(size=x.shape[0])

plt.plot(x,y, '.');

plt.plot(x,y,'.')

xx = x.reshape(-1,1)

for i in [1,2,4,6,8]:

dtsin = DecisionTreeRegressor(max_depth=i)

dtsin.fit(xx, y)

plt.plot(x, dtsin.predict(xx), label=str(i), alpha=1-i/10, lw=i)

plt.legend();

plt.plot(x,y,'.')

xx = x.reshape(-1,1)

for i in [2,4,6,8]:

dtsin = DecisionTreeRegressor(min_samples_split=i)

dtsin.fit(xx, y)

plt.plot(x, dtsin.predict(xx), label=str(i), alpha=1-i/10, lw=i)

plt.legend();

plt.plot(x,y,'.')

xx = x.reshape(-1,1)

for i in [2,4,6,8]:

dtsin = DecisionTreeRegressor(max_depth=6, min_samples_split=i)

dtsin.fit(xx, y)

plt.plot(x, dtsin.predict(xx), label=str(i), alpha=1-i/10, lw=i)

plt.legend();

Ok with this discussion in mind, lets approach Random Forests.

Random Forests¶

Whats the basic idea?

- Decision trees overfit

- So lets introduce randomization.

- Randomization 1: Use bootstrap resampling to create different training datasets. This way each training will give us a different tree and the robust aspects of the regression will remain.

- Added advantage is that the left off points can be used to "validate"

- Just like in polynomials we can choose a large

max_depthand we are ok as we expect the robust signal to remain

plt.plot(x,y,'.')

for i in range(100):

dtsin = DecisionTreeRegressor(max_depth=6)

isamp = np.random.choice(range(x.shape[0]), replace=True, size=x.shape[0])

xx = x[isamp].reshape(-1,1)

dtsin.fit(xx, y[isamp])

plt.plot(x, dtsin.predict(x.reshape(-1,1)), 'r', alpha=0.05)

But this is not enough randomization, because even after bootstrapping, you are mainly training on the same data points, those that appear more often, and will retain some overfitting.

I cant do anything in 1 D but in more than 1D i can choose what predictors to split on randomly, and how many to do this on. This gets us a random forest.

from sklearn.ensemble import RandomForestRegressor

# code from

# Adventures in scikit-learn's Random Forest by Gregory Saunders

from itertools import product

from collections import OrderedDict

param_dict = OrderedDict(

n_estimators = [400, 600, 800],

max_features = [0.2, 0.4, 0.6, 0.8]

)

param_dict.values()

Here we create a Param Grid. We are preparing to use the bootstrap points not used to validate.

max_features : int, float, string or None, optional (default=”auto”)

The number of features to consider when looking for the best split.max_features: Default splits on all the features and is probably prone to overfitting. You'll want to validate on this.- You can "validate" on the trees

n_estimatorsas well but many a times you will just look for the plateau in the trees as seen below. - From decision trees you get the

max_depth,min_samples_split, andmin_samples_leafas well but you might as well leave those at defaults to get a maximally expanded tree.

Using the OOB score.¶

We have been putting "validate" in quotes. This is because the bootstrap gives us left-over points! So we'll now engage in our very own version of a grid-search, done over the out-of-bag scores that sklearn gives us for free

from itertools import product

results = {}

estimators= {}

for n, f in product(*param_dict.values()):

params = (n, f)

est = RandomForestRegressor(oob_score=True,

n_estimators=n, max_features=f, n_jobs=-1)

est.fit(Xtrain, ytrain)

results[params] = est.oob_score_

estimators[params] = est

outparams = max(results, key = results.get)

outparams

rf1 = estimators[outparams]

results

rf1.score(Xtest, ytest)

Since our response is very skewed, we may want to suppress outliers by using the mean_absolute_error instead.

from sklearn.metrics import mean_absolute_error

mean_absolute_error(ytest, rf1.predict(Xtest))

sklearn supports this (criterion='mae') since 0.18, but does not have arbitrary loss functions for Random Forests.

YOUR TURN NOW

Lets try this with MAE

# your code here

Finally you can get feature importances. Whenever a feature is used in a tree in the forest, the algorithm will log the decrease in the splitting criterion such as gini. This is accumulated over all trees and reported in est.feature_importances_

pd.Series(rf1.feature_importances_, index=names).sort_values().plot(kind="barh")

You can do cross-validation if you want, and a cv of 3 will roughly be comparable. But this will take much more time as you are doing the fit 3 times plus the bootstraps. So atleast three times as long!

param_dict2 = OrderedDict(

n_estimators = [600],

max_features = [0.2, 0.4, 0.6]

)

from sklearn.model_selection import GridSearchCV

est2 = RandomForestRegressor(oob_score=False)

gs = GridSearchCV(est2, param_grid = param_dict2, cv=3, n_jobs=-1)

gs.fit(Xtrain, ytrain)

rf2 = gs.best_estimator_

rf2

gs.best_score_

How would you support scoring using mean absolute error if you use cross-validation?

Seeing error as a function of the number of trees¶

We can instead, of different max_features see how performance varies across the number of trees one uses:

# from http://scikit-learn.org/stable/auto_examples/ensemble/plot_ensemble_oob.html

feats = param_dict['max_features']

#

error_rate = OrderedDict((label, []) for label in feats)

# Range of `n_estimators` values to explore.

min_estimators = 200

step_estimators = 200

num_steps = 3

max_estimators = min_estimators + step_estimators*num_steps

for label in feats:

for i in range(min_estimators, max_estimators+1, step_estimators):

clf = RandomForestRegressor(oob_score=True, max_features=label)

clf.set_params(n_estimators=i)

clf.fit(Xtrain, ytrain)

# Record the OOB error for each `n_estimators=i` setting.

oob_error = 1 - clf.oob_score_

error_rate[label].append((i, oob_error))

# Generate the "OOB error rate" vs. "n_estimators" plot.

for label, clf_err in error_rate.items():

xs, ys = zip(*clf_err)

plt.plot(xs, ys, label=label)

plt.xlim(min_estimators, max_estimators)

plt.xlabel("n_estimators")

plt.ylabel("OOB error rate")

plt.legend(loc="upper right")

plt.show()

Gradient Boosted Regression Trees¶

Adaboost Classification, which you will be doing in your homework, is a special case of a gradient-boosted algorithm. Gradient Bossting is very state of the art, and has major connections to logistic regression, gradient descent in a functional space, and search in information space. See Shapire and Freund's MIT Press book for details.

But briefly, let us cover the idea here. The idea is that we will use a bunch of weak learners and fit sequentially. The first one fits the signal, the second one the first residual, the third the second residual and so on. At each stage we upweight the places that our previous learner did badly on. First let us illustrate.

from sklearn.ensemble import GradientBoostingRegressor

estgb = GradientBoostingRegressor(n_estimators=500, max_depth=1, learning_rate=1.0)

estgb.fit(x.reshape(-1,1), y)

staged_predict_generator = estgb.staged_predict(x.reshape(-1,1))

# code from http://nbviewer.jupyter.org/github/pprett/pydata-gbrt-tutorial/blob/master/gbrt-tutorial.ipynb

import time

from IPython import display

plt.plot(x, y, '.');

i = 0

counter = 0

for stagepred in staged_predict_generator:

if i in [0, 1, 2, 4, 8, 20, 50, 100, 200, 400, 500]:

plt.plot(x, stagepred, alpha=0.7, label=str(i), lw=2)

plt.legend();

display.display(plt.gcf())

display.clear_output(wait=True)

time.sleep(2 - counter*0.1)

counter = counter + 1

i = i + 1

Ok, so this demonstration helps us understand some things about GBRT.

n_estimatorsis the number of trees, and thus the stage in the fitting. It also controls the complexity for us. The more trees we have the more we fit to the tiny details.staged_predictgives us the prediction at each step- once again

max_depthfrom the underlying decision tree tells us the depth of the tree. But here it tells us the amount of features interactions we have, not just the scale of our fit. But clearly it increases the variance again.

Ideas from decision trees remain. For example, increase min_samples_leaf to increase the bias.

YOUR TURN NOW

Demonstrate what happens when you increase

max_depthto 5

# your code here

YOUR TURN NOW

What happens if you put

max_depthback to 1 and decrease the learning rate to 0.1?

# your code here

Whats the relationship between residuals and the gradient?¶

Pavlos showed in class that for the squared loss, taking the gradient in the "data point functional space", ie a N-d space for N data points with each variable being $f(x_i)$ just gives us the residuals. It turns out that the gradient descent is the more general idea, and one can use this for different losses. And the upweighting of poorly fit points in AdaBoost is simply a weighing by gradient. If the gradient (or residual) is high it means you are far away from optimum in this functional space, and if you are at 0, you have a flat gradient!

The ideas from the general theory of gradient descent tell us this: we can slow the learning by shrinking the predictions of each tree by some small number, which is called the learning_rate (learning_rate). This "shrinkage" helps us not overshoot, but for a finite number of iterations also simultaneously ensures we dont overfit by being in the neighboorhood of the minimum rather than just at it! But we might need to increase the iterations some to get into the minimum area.

Ok, so how to do the fit?¶

gb = GradientBoostingRegressor(n_estimators=1000, max_depth=5)

gb.fit(Xtrain, ytrain)

A deviance plot can be used to compare train and test errors against the number of iterations.

- Training error (deviance, related to the KL-divergence) is stored in

est.train_score_ - Test error is computed using

est.staged_predict(this usesest.loss_)

def deviance_plot(est, X_test, y_test, ax=None, label='', train_color='#2c7bb6',

test_color='#d7191c', alpha=1.0, ylim=(0, 10)):

"""Deviance plot for ``est``, use ``X_test`` and ``y_test`` for test error. """

n_estimators = len(est.estimators_)

test_dev = np.empty(n_estimators)

for i, pred in enumerate(est.staged_predict(X_test)):

test_dev[i] = est.loss_(y_test, pred)

if ax is None:

fig = plt.figure()

ax = plt.gca()

ax.plot(np.arange(n_estimators) + 1, test_dev, color=test_color, label='Test %s' % label,

linewidth=2, alpha=alpha)

ax.plot(np.arange(n_estimators) + 1, est.train_score_, color=train_color,

label='Train %s' % label, linewidth=2, alpha=alpha)

ax.set_ylabel('Error')

ax.set_xlabel('n_estimators')

ax.set_ylim(ylim)

return test_dev, ax

deviance_plot(gb, Xtest, ytest, ylim=(0,0.8));

plt.legend();

Notice the wide gap. This is an indication of overfitting!

Unlike random forests, where we are using the randomness to our benefits, the GBRT requires careful cross-validation

Peter Prettenhofer, who wrote sklearns GBRT implementation writes in his pydata14 talk (worth watching!)

Hyperparameter tuning I usually follow this recipe to tune the hyperparameters:

- Pick n_estimators as large as (computationally) possible (e.g. 3000)

- Tune max_depth, learning_rate, min_samples_leaf, and max_features via grid search

- A lower learning_rate requires a higher number of n_estimators. Thus increase n_estimators even more and tune learning_rate again holding the other parameters fixed

This last point is a tradeof between number of iterations or runtime against accuracy. And keep in mind that it might lead to overfitting.

Let me add however, that poor learners do rather well. So you might want to not cross-validate max_depth. And min_samples_per_leaf is not independent either, so if you do use cross-val, you might just use one of those.

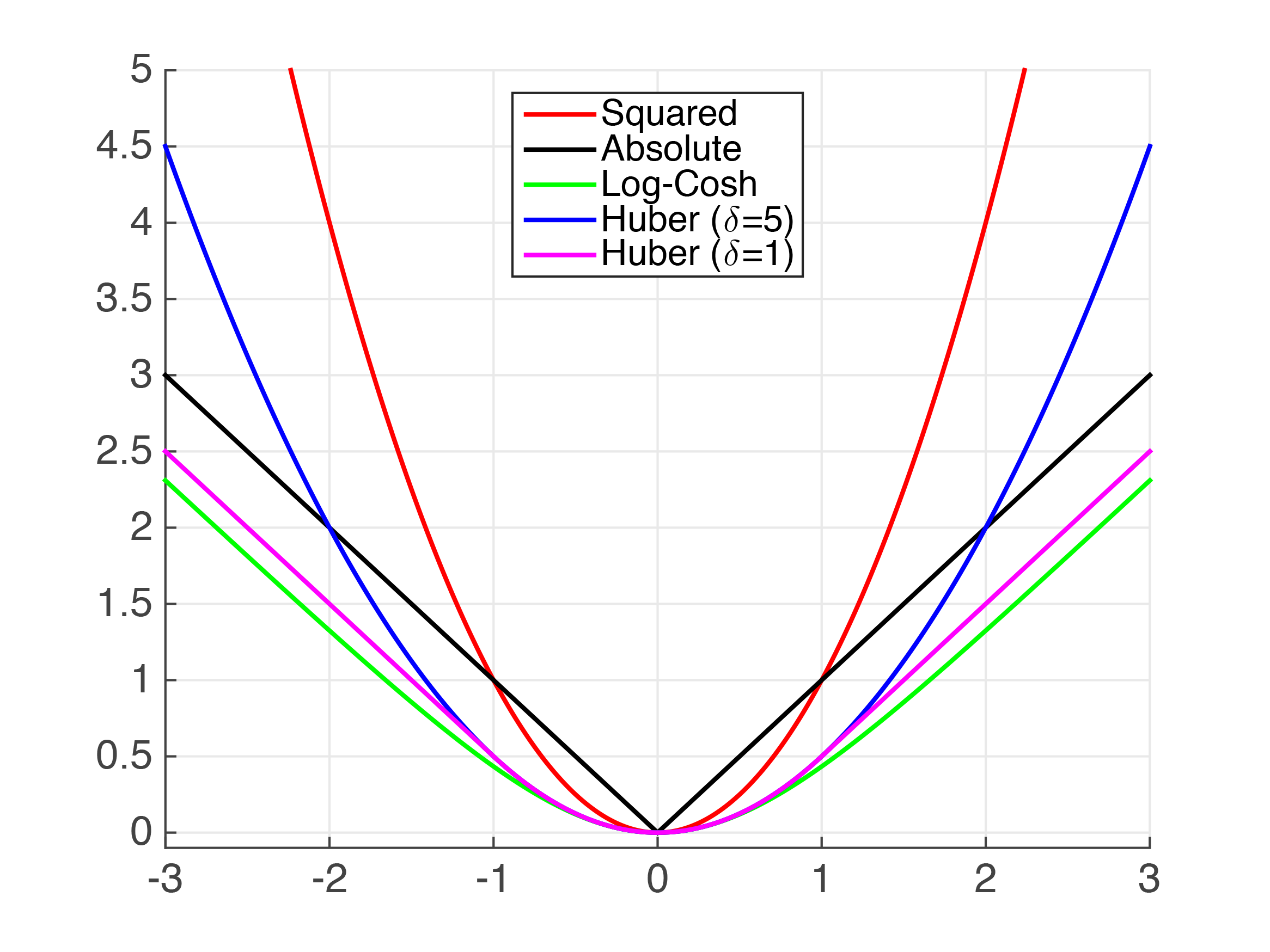

Cross Validation with Huber Loss¶

The Huber Loss may be used to deal with outliers. Here is a diagram from Cornell's CS4780:

param_grid = {'learning_rate': [0.1, 0.01],

'max_depth': [3, 6],

'min_samples_leaf': [3, 5], ## depends on the num of training examples

'max_features': [0.2, 0.6]

}

gb = GradientBoostingRegressor(n_estimators=600, loss='huber')

gb_cv = GridSearchCV(gb, param_grid, cv=3, n_jobs=-1)

This will take some time! We've made a smaller grid, but things are still slow

gb_cv.fit(Xtrain, ytrain)

gb_cv.best_estimator_

We get a slightly better MAE than Random Forest, even though the model scoring was done on mean squared error. There is a price to be paid, however, time costly cross-validation.

Notice that the criterion on the splits uses a specific MSE, and we did not score on cross-validation by another loss, simply using MSE.

mean_absolute_error(ytest, gb_cv.predict(Xtest))

And the deviance plot shows a huge narrowing of the gap!

deviance_plot(gb_cv.best_estimator_, Xtest, ytest, ylim=(0,0.8));

plt.legend();

bp = gb_cv.best_params_

bp

We can now play with the number of iterations and the learning rate.

param_grid2 = {'learning_rate': [0.1, 0.01, 0.001]}

gb2 = GradientBoostingRegressor(n_estimators=1000,

loss="huber",

max_depth=bp['max_depth'],

max_features=bp['max_features'],

min_samples_leaf=bp['min_samples_leaf'])

gb2_cv = GridSearchCV(gb2, param_grid2, cv=3, n_jobs=-1)

gb2_cv.fit(Xtrain, ytrain)

gb2_cv.best_estimator_

mean_absolute_error(ytest, gb2_cv.predict(Xtest))

deviance_plot(gb2_cv.best_estimator_, Xtest, ytest, ylim=(0,0.8));

plt.legend();

We are slightly better. Feature importances again:

pd.Series(gb2_cv.best_estimator_.feature_importances_, index=names).sort_values().plot(kind="barh")

Tips:¶

- ordinal encoding in trees for categorical variables is as effective as one-hot encoding but more efficient, using less memory and being faster. But your trees need to be deeper as you are making more cuts

- often explicit interactions are useful in GBRT even tho it detects interactions

YOUR TURN NOW

Repreat the process using the Huber loss and the MAE for scoring